Good news this morning for our Variable Rate Mortgage holders and anyone with a loan attached to the Prime rate. Today it was cut by .50% effective tomorrow which in turn will lower mortgage and loan payments. For those with static payments, such as mortgages with TD, RBC and others, you will now be paying more towards the principal and less to interest. Below is the news release from DLC’s own economist, Dr. Sherry Cooper.

If you want help or advice for anything mortgage related or how these rate cuts affect you, please connect with us at the office and we would love to chat more with you about it.

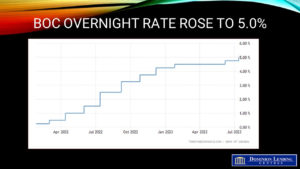

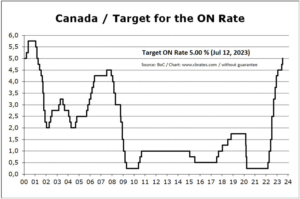

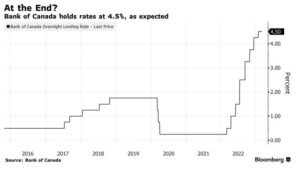

The BoC slashed the overnight rate by 50 bps this morning, bringing the policy rate down to 3.25%. The market had priced in nearly 90% odds of a 50 bp move, where consensus coalesced. The combined slower-than-expected GDP growth and a sharp rise in the Canadian unemployment rate to 6.8% triggered the Bank’s second consecutive jumbo rate cut. Today’s move will take the prime rate down 50 bps to 5.45% effective tomorrow, reducing floating rate mortgage loan rates by a half point, easing the cost of borrowing and reducing the monthly payment increase for renewals. This should spark housing activity, which accelerated in October and November.

The policy rate is now at the top of the estimated neutral rate range, 2.25% to 3.25%, with more moderate rate cuts continuing into next year. However, monetary policy remains restrictive, as the 3.25% policy rate is still 125 basis points above inflation, which has declined to roughly 2%, the Bank’s inflation target.

Economists have suggested that the tone of the central bank’s press release is more hawkish than before, unsurprising following two consecutive jumbo rate cuts. The Bank continues to say that its future decisions are data-dependent and will be impacted by policy measures taken by the government. In particular, the Bank highlighted the coming GST cuts, dispersal of bonus checks and the significant reduction in immigration. These developments have offsetting implications for inflation.

Governor Macklem signaled that he anticipated “a more gradual approach to monetary policy” in his press conference. We are forecasting 25 bp rate cuts through at least the first half of next year. That would take the overnight rate down to 2.5% by early June, a huge boost to housing that will likely enjoy a strong spring season.

Bottom Line

Today’s action is great news for the Canadian economy and housing activity. The central bank said that planned immigration target reductions are the “most significant” factor for the 2025 outlook and suggest below-forecast GDP growth. However, the “effects on inflation will likely be more muted, given that lower immigration dampens both demand and supply.” Lower immigration is one of the “factors” that caused the BoC to cut 50 bps and not 25, Macklem said.

During this cycle, the Bank of Canada has been the most aggressive central bank in cutting rates. Even so, the Canadian dollar edged higher following the Bank’s announcement, likely because markets now expect a more moderate pace of rate reduction next year.