The Bank of Canada was expected to raise rates another .25% higher, and that is exactly what was announced this morning. The policy rate is now 4.50%, the highest rate since 2007. Which is the bank’s 8th consecutive rate hike in the past year, but the smallest one yet.

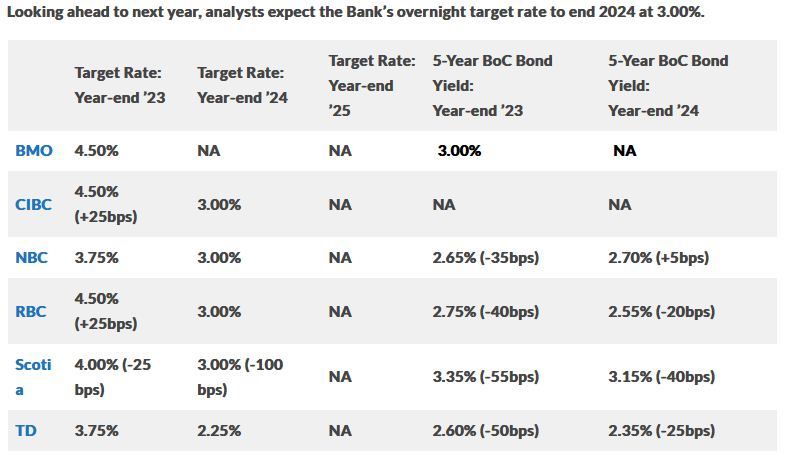

Some have predicted that for the year of 2023 the rates will continue to trend upward, but the Bank of Canada stated today that this could be the peak for this current tightening cycle as inflation is expected to “decline significantly” in the upcoming months. For Canadians, this means an extra $15.67 added to your mortgage payment for every $100,000 in mortgage.

“We’ve raised rates rapidly, and now it’s time to pause and assess whether monetary policy is sufficiently restrictive to bring inflation back to its two per cent target,” Bank of Canada Governor Tiff Macklem told reporters after the rate announcement.

As of this January, there is an agreement between the big banks that in 2023 a recession will happen in Canada. Although economists are saying that this recession would likely be mild to moderate in comparison to previous recessions.

The banks have a real-time view of cardholder spending data and are well-positioned to report on economic trends sooner, and what we are learning is that spending is decreasing significantly due to higher costs throughout the economy and with higher interest rate expenses, we are at the point of an overall economic slowdown. But with lower spending comes a slowing economy and lower inflation, and eventually, lower mortgage interest rates.

At this time of higher rates, there is no good low rate to lock into. With this said, a calculated approach should be considered to position yourself to take advantage of lower rates once they begin to fall. Therefore a shorter term on your mortgage such as a 3 year fixed rate, could position you better to renew into a lower fixed rate in 3 years’ time. The typical 5 year term may be too long for a higher rate.

But for those with a higher tolerance to risk, a variable rate may be worth considering. Given over 40 years of rate data, as seen in a York University study on Canadian interest rates, the variable rate is likely to lead to more significant savings over years. As soon as the rate begins to fall, as predicted to in late 2023 or early 2024, the variable rate holder will benefit immediately. This ‘lower rate sooner’ potential could lead to more savings than locking in even a shorter term fixed rate. But with variable rates higher currently and another 0.25% increase announced today, it will take a strong willed person in 2023 to realize these savings over the next few years.

Have any more questions about what this means for you and your family? Don’t hesitate to reach out to us at Primex Mortgages, we would be more than happy to chat!

Trish & The Primex Team